![]() Teva’s strategy to boost its operational efficiency and tap strategic partnerships seems to be paying off. In its Q3 earnings report, Teva announced that global revenues were up to $3.9 billion, marking a 7% rise from the previous year’s third quarter. Factors fueling the growth include the robust performance of their specialty medications, Austedo and Ajovy, as well as a strong showing from their generics portfolio. However, despite these promising stats, investors appear to be cautious. Teva’s stock is down almost 8% so far this year, currently trading at $8.77.

Teva’s strategy to boost its operational efficiency and tap strategic partnerships seems to be paying off. In its Q3 earnings report, Teva announced that global revenues were up to $3.9 billion, marking a 7% rise from the previous year’s third quarter. Factors fueling the growth include the robust performance of their specialty medications, Austedo and Ajovy, as well as a strong showing from their generics portfolio. However, despite these promising stats, investors appear to be cautious. Teva’s stock is down almost 8% so far this year, currently trading at $8.77.

For Austedo, Sven Dethlefs, the company’s head of North America commercial, noted that the company has seen growth for the extended-release version of the drug. In an earnings call, Dethlefs said the company has seen “a significant number of new prescribers that have never prescribed Austedo before that now start prescribing Austedo XR.” He added that the demand for the XR version of the drug puts the company on the right track in “making Austedo a continuous growth driver” for its business.

A rosy outlook for 2024

The company bolstered its outlook for 2024, forecasting its revenue to fall in the range of $15.1 to $15.5 billion. Factors behind the optimistic projection include an exclusive deal with Sanofi aimed at developing and commercializing new treatments. The company has also made progress with its “Pivot to Growth” strategy, which involves fortifying its commercial offerings with profitable drugs and biosimilars. Other pillars of the strategy include homing in on neuroscience and immunology, sustaining its established presence in the generics marketplace, and allocating capital to fuel these areas of growth.

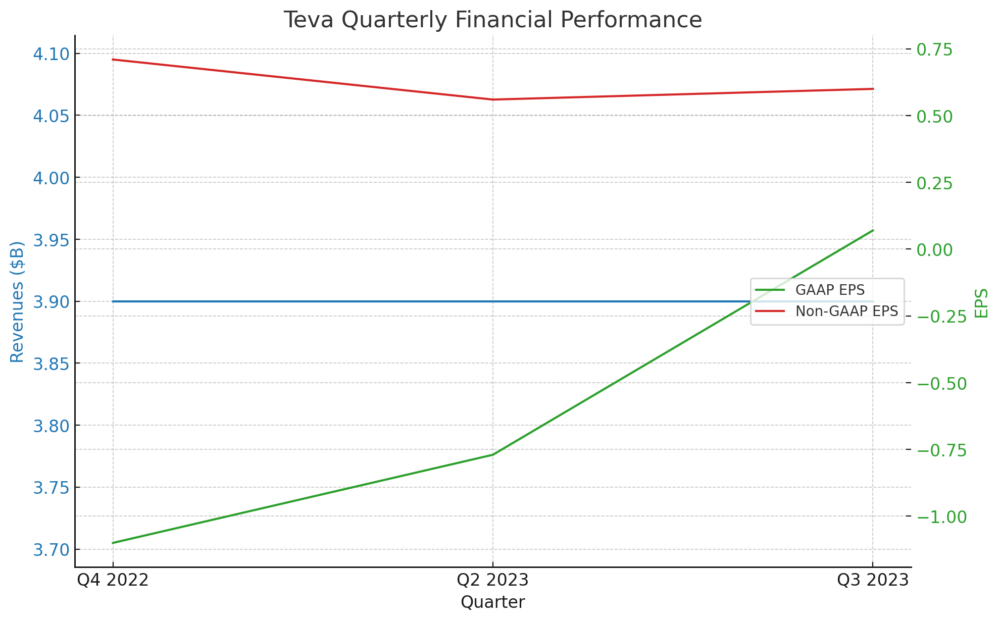

Financial performance in context

With this “Pivot to Growth” strategy, Teva projects to surpass annual revenues of $2.5 billion from Austedo alone by 2027.

The graph below charts revenues alongside GAAP and non-GAAP earnings-per share (EPS).

Given the current war in Israel, Teva has introduced a proactive strategy to ensure the safety and well-being of its workforce while maintaining its operational commitments.

Although Teva has projected growth into 2024, the company’s stock has fallen considerably since its peak in 2015, when it hit a high closing price of $67.06 on July 27, 2015. A number of factors are at play in the decline, including a considerable debt burden, legal entanglements, and challenges in converting earnings into free cash flow. As of mid-2021, Teva carried net debt of about $22.7 billion, and while the debt levels have been decreasing, they still constrain the company. In addition, Teva has faced a number of legal woes, ranging from patent disputes to the opioid litigation. In 2022, Teva joined Allergan (now a unit of AbbVie) in agreeing to pay $5B billion to settle opioid allegations.

Tell Us What You Think!